Experienced stock traders often associate market corrections with an increase in metrics like the VIX index, which measures volatility expectations. However, the dynamics in the bitcoin market present a different scenario.

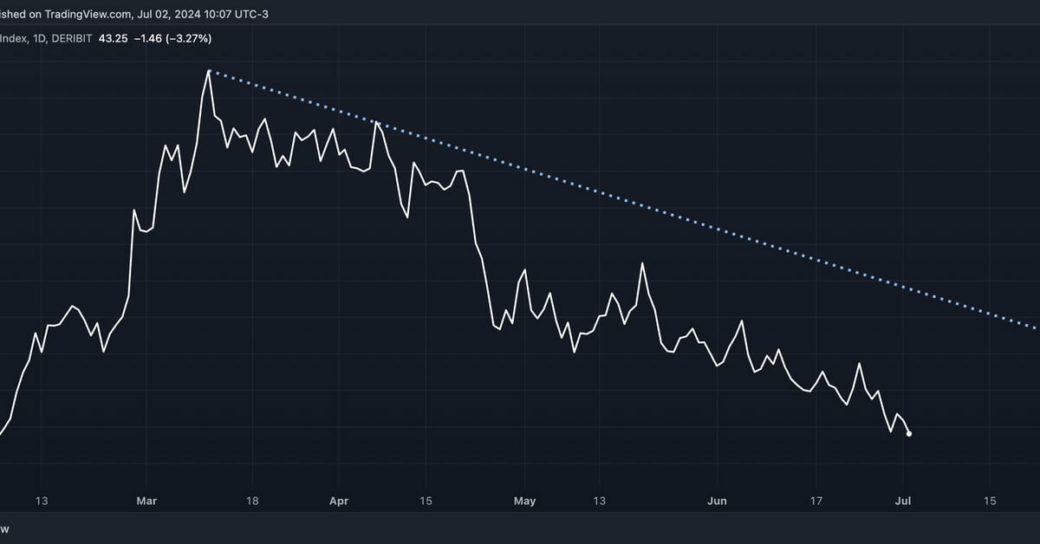

Despite the usual positive correlation between cryptocurrency prices and tech stocks, the recent 10% pullback in bitcoin’s price from over $70,000 in the past four weeks did not result in an expected surge in volatility metrics like the Deribit’s bitcoin volatility index DVOL.

DVOL, an options-derived measure of expected price turbulence over the next 30 days, has actually decreased from an annualized 53% to 42%, hitting its lowest level since early February. This decline in implied volatility suggests a relatively calm market environment where investors are less inclined to panic or engage in protective strategies.

Implied volatility is influenced by the demand for options contracts that allow the buyer to purchase or sell the underlying asset at a predetermined price in the future. In the case of bitcoin, the decrease in DVOL despite the price correction indicates a lack of appetite for buying volatility, especially with the market exhibiting slow and orderly movement rather than sharp declines.

According to David Brickell, head of international distribution at crypto platform FRNT Financial, the subdued market conditions have led to a trend of volatility selling, where investors sell options in a stable market environment to decrease implied volatility. This strategy often involves writing call options on existing holdings.

Brickell suggests that a potential resurgence in bitcoin’s price, surpassing $70,000, could reignite interest in options trading and raise the DVOL index. He points out that throughout the current bull cycle, bitcoin’s price has shown a positive correlation with the DVOL index.

To break out of the current volatility lull, Brickell anticipates that bitcoin would need to test higher levels and potentially threaten a significant breakout. This shift in market dynamics could prompt investors to reevaluate their options strategies and lead to increased demand for volatility products.