Marathon Digital Follows MicroStrategy’s Bitcoin Accumulation Strategy

Billionaire Michael Saylor was a pioneer in large-scale corporate investments in bitcoin (BTC), utilizing borrowed funds to transform his company, MicroStrategy (MSTR), into one of the largest corporate holders of this cryptocurrency. Recently, a surprising company has adopted a similar strategy—not in software development, but in the bitcoin mining industry. Marathon Digital Holdings (MARA) has taken a bold step by selling debt to finance the acquisition of bitcoin instead of using borrowed money to expand its mining operations.

This approach highlights the challenges facing the mining sector in 2023. Marathon Digital recently raised $300 million through the sale of convertible notes, which are bonds convertible into company stock. With these funds, Marathon purchased 4,144 bitcoin, a strategic decision that reflects the tough conditions currently experienced in the mining industry.

Marathon’s decision to invest in bitcoin rather than expand its mining capacity is largely influenced by the current market conditions. The company stated, “Given the current mining hash price, the internal rate of return (IRR) indicates that purchasing bitcoin using funds from debt or equity issuances is more beneficial to shareholders until conditions improve.” The term “hash price” refers to a metric that evaluates mining profitability and has been under pressure due to increasing competition and operational costs.

MicroStrategy’s Journey: A Cautionary Tale or a Blueprint for Success?

MicroStrategy’s strategy of accumulating bitcoin faced significant criticism when the cryptocurrency’s price plunged in 2022, leaving the company’s investments temporarily underwater. However, as the market recovered, MicroStrategy’s substantial bitcoin holdings appreciated significantly, now valued at billions more than their initial purchase prices. This turnaround has led many to reconsider Saylor’s approach as a potential blueprint for other companies in the industry.

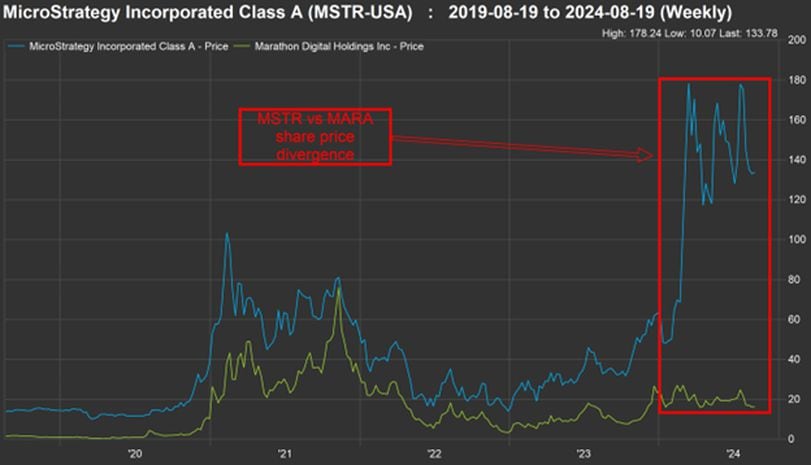

Both MicroStrategy and Marathon have seen their stock prices act as proxies for bitcoin’s price movements since Saylor began buying in 2020. However, the stock market trajectories of both companies have diverged significantly in 2023. MicroStrategy’s stock surged by 90%, closely tracking bitcoin’s price, while Marathon’s stock fell by approximately 40%. This decline stems from the challenges faced by the mining sector, particularly following the Bitcoin halving event in April, which reduced the reward for mining new bitcoin by half and dramatically impacted miners’ revenues.

Marathon’s Shift to a Full HODL Strategy

In response to the adverse market conditions, Marathon Digital has adopted a “full HODL” strategy, which entails holding onto all the bitcoin it mines rather than selling it. This strategy reflects a strong belief in the long-term value of bitcoin. Fred Thiel, Marathon’s chairman and CEO, stated, “We believe bitcoin is the world’s best treasury reserve asset and support the idea of sovereign wealth funds holding it. We encourage governments and corporations to all hold bitcoin as a reserve asset.”

Following the adoption of this strategy, Marathon announced its $300 million debt offering to purchase more bitcoin. Currently, the company owns over 25,000 bitcoin, making it the second-largest corporate holder of bitcoin after MicroStrategy. This significant acquisition underlines Marathon’s commitment to accumulating bitcoin in a market environment that is becoming increasingly challenging for miners.

The Profit Squeeze in Bitcoin Mining

The stark difference in share price performance between MicroStrategy and Marathon is not surprising given the current struggles within the mining industry. This sector is facing overcrowding, heightened competition, and escalating operational costs. Furthermore, the Bitcoin network’s hashrate and difficulty levels are increasing, making it even harder for miners to create new bitcoin.

JPMorgan has reported that mining profitability has reached all-time lows, with the network’s hashrate increasing significantly. The hashprice—the average reward miners earn per unit of computational power—is still around 30% lower than it was in December 2022 and approximately 40% below pre-halving levels. Many miners are now shifting from being solely focused on mining to diversifying into other ventures, such as artificial intelligence, to ensure their survival in this challenging landscape.

- Swan Bitcoin recently canceled its IPO and scaled back its mining operations due to a lack of revenue.

- Galaxy Research noted that while some miners can still generate positive gross profits, many are becoming unprofitable when factoring in operating expenses.

Institutional Investment Strategies and Debt Financing

The introduction of bitcoin exchange-traded funds (ETFs) in the U.S. has provided institutional investors with a more direct avenue for cryptocurrency exposure, diminishing the appeal of investing in bitcoin miners. As a result, many institutional investors have developed a strategy of shorting miners while going long on ETFs, effectively capping the miners’ share price appreciation.

To remain competitive and navigate this financial squeeze, miners like Marathon face limited choices. They can either invest heavily in their capital-intensive operations or pursue acquisitions, both of which entail significant risk and time commitments. This environment has led Marathon to take a page from MicroStrategy’s successful playbook by purchasing bitcoin directly from the open market.

Marathon’s statement reflects this strategy: “During periods of significant price appreciation, we may focus solely on mining. However, with bitcoin trending sideways and costs increasing, we expect to opportunistically ‘buy the dips.'” This approach aligns with the broader trend in the mining sector, where companies are increasingly focusing on accumulating bitcoin to capture potential future value.

Convertible Debt: A Strategic Move for Future Growth

Marathon’s use of convertible senior notes to finance its bitcoin purchases is a noteworthy development. Unlike traditional debt, these notes can be converted into equity, allowing Marathon to raise capital while minimizing immediate dilution of shareholders’ equity. The company offered these notes at a low interest rate of 2.125%, which is lower than the current 10-year U.S. Treasury rate of 3.84% and comparable to MicroStrategy’s recent offerings.

This strategic maneuver not only allows Marathon to take advantage of potential upside in bitcoin prices but also prepares the company for future acquisitions in a consolidating mining industry. As Ethan Vera, COO of Luxor Tech, noted, “Adding a Bitcoin balance sheet position allows companies to raise capital with a clear use of funds while preparing their balance sheet for potential M&A.” This indicates a shift in the mining industry’s landscape, where companies are beginning to embrace debt financing once again after a period of reluctance following the 2022 market downturn.

In conclusion, Marathon Digital’s recent actions reflect the growing complexities of the bitcoin mining industry amid shifting market dynamics. The company’s choice to adopt a strategy similar to MicroStrategy’s, focusing on bitcoin accumulation through convertible debt, positions it to navigate the current challenges while maximizing potential future gains. As competition intensifies and operational costs rise, innovative financial strategies will be vital for the survival and growth of companies in this evolving sector.